"Say Hello to

Independent Financial Advice"

0191 281 8811

Client Login

0191 281 8811

Client Login

Cashflow planning: how it could help you achieve your retirement goals

Will you retire when you want, with the lifestyle you’re accustomed to? After all, retirement is a major life event, one which many of us dream about for most of our working life. Whether you want to spend your retirement travelling, making memories with friends and family, or enjoying hobbies, old and new – it’s important to have a goal in mind and a plan in place to help make it a reality.

Our sophisticated cashflow modelling software takes into consideration the wealth a client has accumulated, and it crunches the numbers, including anticipated rates of investment and savings growth, as well as inflation. It’s an invaluable way of building a picture of how their wealth could last over their retirement and highlight any potential shortfalls – ultimately helping us to determine if more needs to be done to help the client achieve the retirement they want.

Benefits of cashflow planning

- It gives you a visual representation of your financial future

It can be difficult to understand how your retirement provisions will change over time; particularly when you begin to factor in areas such as investment growth and inflation. Cashflow modelling helps to forecast how your wealth will stand the test of time in a visual and easy to digest way. This makes it far easier to grasp the bigger picture.

It will showcase where you are now, how your wealth may be affected over time, the level of income you can afford to take in retirement, whilst taking into consideration the age you wish to retire. You might be pleasantly surprised by the possible date that you could comfortably retire, or shortfalls could be identified, which will help us to put steps in place to increase your funds before retiring.

- It gives you an insight into how life events could impact your finances

Let’s face it, life rarely goes to plan, and that doesn’t change in retirement. Even with work out of the picture, you’re likely to experience big life events which will inevitably influence your finances and retirement plans. When building your cashflow plan, we can develop various scenarios which take into account your goals and consider possible events that could occur during your retirement.

This will enable us to gain an understanding of the potential impact of these events on your income. These events could include planned decisions, such as downsizing, or situations which may happen, for example, receiving an inheritance or going into long-term care.

Using cashflow planning can show if your retirement aspirations could be achievable, helping you to make a more informed decision when it comes to your retirement plan. But it goes beyond that. It’s a process that can give you reassurance that there are steps you can take to overcome life’s financial obstacles once you retire.

Let’s take a look at an example:

Our client is aged 56 and has the aspiration to retire at 60 with a £2,250 per month income throughout their retirement. Our client is currently working full time, earning £40,000 a year and has no liabilities.

To build a picture of what their retirement could look like, based on their goals, we will take into account the range of finances and assets the client has, to get a comprehensive picture of their wealth. This will include property, pensions, savings, investments, and any other wealth they may have.

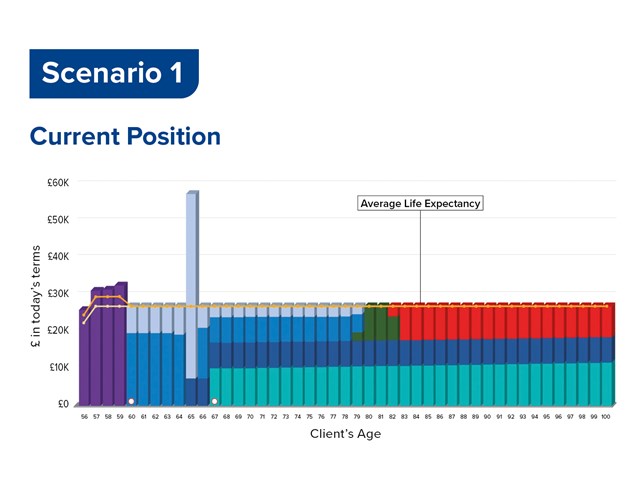

Scenario 1

The diagram above forecasts how the client’s retirement could look if they were to retire at 60 in their current position. As you can see, the client receives a salary until retirement at 60, then their income comes mainly from tax free cash and withdrawals from their personal pension until they are entitled to receive payments from their final salary pension and the state pension at age 67.

However, as highlighted by the blocks in red, the cashflow modelling establishes that the client is likely to have an income shortfall from aged 82, based on the various assumptions considered, and therefore retiring at 60 may not be in their best interest.

However, there are always options available and a financial adviser can help you to make an informed decision on which one is the most suitable for you and your circumstances. They will also complete a pension review to ensure your pension provisions are aligned to your retirement goals.

Options the client could consider from here:

- Delay retirement: A couple of years can make all the difference to your retirement outcome.

- Reduce retirement income: Consider whether you need that level of income every month, reducing your required income could help your money last longer.

- Phase into retirement: Reducing the amount of days or hours you work could help to cover any shortfall. You will also be making contributions during this time, helping to grow your pension pot.

- Increase your pension contributions: If you are able to, increasing your pension contributions will increase your pension savings, and can offer tax relief on your earnings.

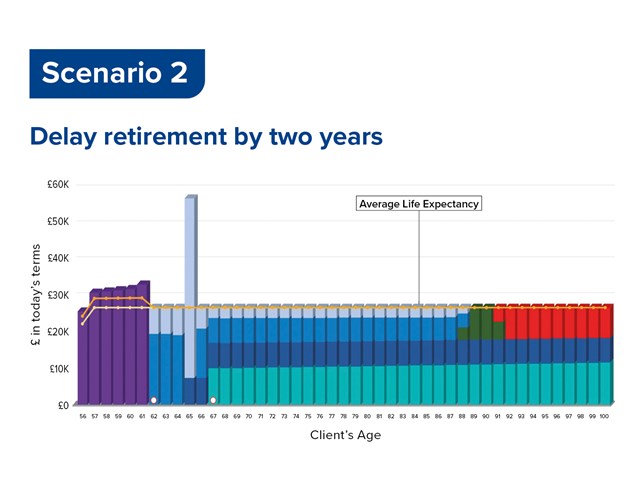

Scenario 2

By delaying retirement until 62, the client would benefit from a further two years of salary, pension contributions and possible additional growth within their investment portfolio.

As you can see, the client wouldn’t start to run out of money until the age of 90. We could also look to factor in a reduction in income as the client heads towards the later stages of retirement, as they may no longer require the desired income of £2,250.

One of the key benefits of cashflow planning is its ability to stress test your finances, covering a wide range of eventualities, such as a market crash.

For example, if the client was planning to retire, but a market crash happened, cashflow modelling could help to forecast the impact this could have on their finances long-term, enabling them put steps into place to prevent a shortfall later in life.

Here are some of the options the client could consider if a market crash were to occur:

- Potentially downsizing or using equity release to generate capital to be used for retirement income shortfall.

- Delay retirement

- Reduce retirement income

- Phase into retirement

- Increase pension contributions

No one can predict the future, and cashflow modelling is no different. Although a useful tool for painting a picture of what your retirement could look like and considering how your assets could be utilised, there are no guarantees it will play out that way.When making big financial decisions, cashflow planning is just one of the many tools an independent adviser can use, and here at Lowes we take a holistic approach to financial planning, reviewing all your assets and wealth to ensure your money is in the best place to support your long-term financial goals.If you’re looking to build a retirement fund, ready to access your pension savings or want to understand your pension options, we can build a bespoke financial plan which will help you achieve the retirement you want. |

Subscribe Today

Receive exclusive

financial insights

straight to your inbox

We will use the information you have provided only to contact you in accordance to terms of this contact form and our privacy policy.

You can unsubscribe at any time by emailing enquiry@lowes.co.uk or by clicking the 'unsubscribe' link at the bottom of each email. Full details of how we use and secure your personal information and how to update your marketing preferences can be viewed in our Privacy Policy.